Sunday, October 5, 2025

An action-driven community of investors, innovators, and industrials is scaling artificial intelligence (AI) to accelerate the clean economy transition through the global CleanAI Initiative, with locations in Toronto, London, San Francisco and Singapore.

On July 23, 2025, CleanTech North hosted a webinar featuring Emily MacIntosh, Director of Knowledg, and Shivani Chotalia, AI & Climate Lead. A State of Clean AI report was previewed alongside cleantech industry pioneer and founder of the CleanAI Initiative, Nick Parker. Over the course of the hour, they distilled the key findings and trends from the upcoming annual report and highlighted practical takeaways for operators, investors and policymakers.

State of Clean AI Takeaways

The presenters contrasted clean tech (renewables, circular manufacturing, low-carbon materials) with AI (data-driven pattern-discovery and system-optimization) and explained how their overlap—Clean AI—unlocks new scale in climate action: from AI-guided materials discovery for carbon capture to grid-edge energy optimization and remote biodiversity monitoring.

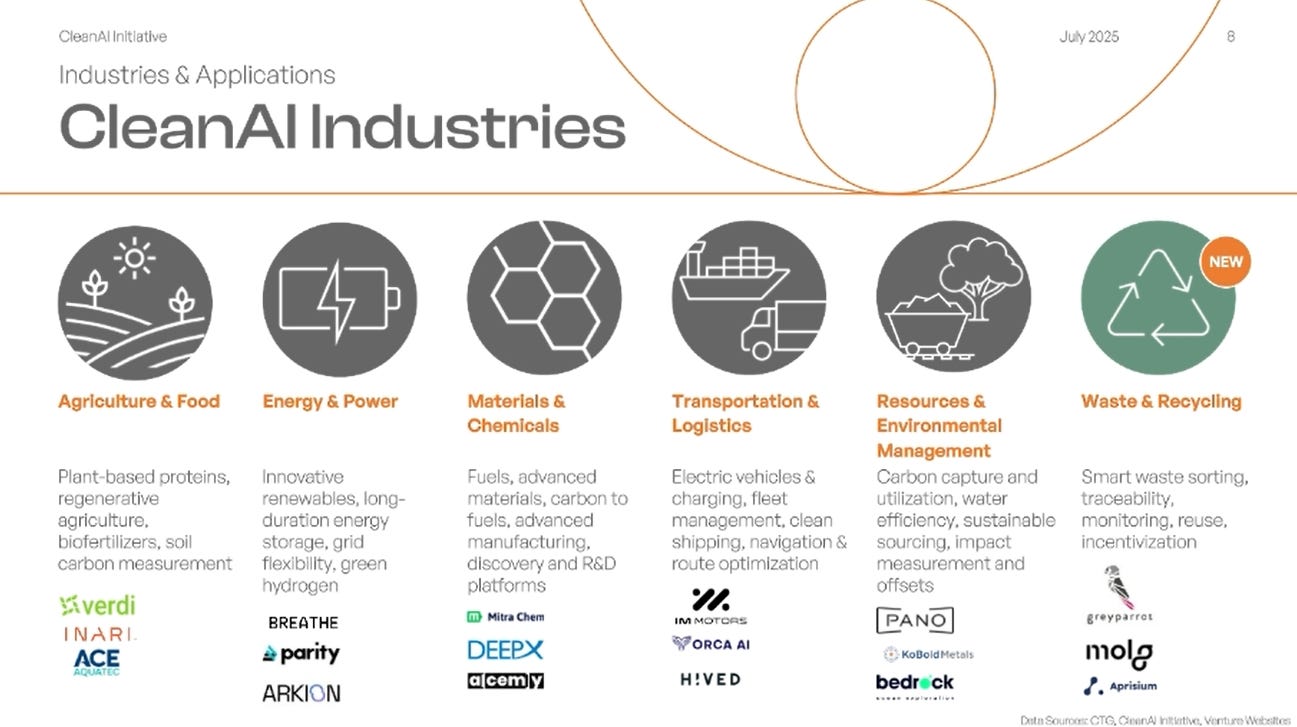

The six high-velocity subsectors were defined and examples of each were provided as follows:

- Energy & Power (47 per cent of clean-AI VC flow): grid-edge software (e.g., Breathe Battery, Parity HVAC) delivering 5–10 GW of “virtual capacity.”

- Materials & Chemicals (fastest YoY growth): generative design platforms (MitraChem, DeepX, EMI’s €15 M aluminium seed) slashing R&D cycles and embodied carbon.

- Agri-Food: autonomous irrigation (Verdi), AI-driven gene-editing (Inari) and aquaculture monitoring (Ace AquaTech) cutting input waste by more than 25 per cent.

- Transport & Logistics: marine-autonomy and collision-avoidance (Orca AI), profitable all-electric last-mile (Hived), and premium AI-powered EV brands (IM Motors).

- Resources & Environmental Management: real-time wildfire detection (Pano AI), seafloor mapping via AUVs (Bedrock Ocean), and mineral-site identification (Cobalt Metals).

- Waste & Recycling: AI-based sorting (Greyparrot), contamination monitoring (Aprisium), and autonomous disassembly of e-waste (Molg)

Investment Momentum & Metrics

- US$50 billion in clean-AI VC since 2020, on track to exceed US $60 billion by 2026.

- 67 per cent surge in AI-related data-center build-out over the past two years—demand projected at 200 GW by 2030.

- AI-driven industrial optimizations could abate 40–70 Mt CO₂e/yr.

- Deal evolution: median round stable at US $4 M; mega-rounds (US $100 M+) rose to 38 in 2024.

- Sectoral split: Energy & Power (47%), Materials & Chemicals (83% YoY growth), with early-stage rounds dominating volume but larger cheques in Seed-to-Series A.

Geographic Dynamics

- United States leads with US $15.5 B across 63 deals.

- Asia (Singapore, Japan, South Korea) driving sovereign AI-compute funds, luring Series B fabs.

- EU has earmarked €200 B for “Invest AI” industrial decarbonization, while emerging-market digital inequity risks widening.

What’s Next?

- Hardware Eats Carbon: on-device inference chips cutting AI power draw by 60–70 per cent.

- Virtual Infrastructure: AI models on grid, HVAC, and fleets unlocking bankable capacity.

- Equity as Infrastructure: compute access as an economic resilience metric—cross-border partnerships vital to inclusive scaling.

The preview made clear that Clean AI is transitioning from niche pilots to core infrastructure. The most successful operators, investors and policymakers will embed AI as a structural lever—designing for water, power and equity constraints and harnessing AI’s exponential potential across materials, molecules and megawatts.

To register for the upcoming CleanAI Summit, visit: Get them at: https://lu.ma/k2kl6v5z

(Note: The EARLYBIRD ticket expires on August 8th.)

Featured image credit: Getty Images